MAURITIUS: Private Trust Companies

The Private Trust Company (“PTC”) can be used within trust structures for holding and managing assets of a family as trustees of family trusts for estate planning purposes. The family members may be appointed on the Board of the PTC and thus exercise a considerable degree of control over their future legacy.

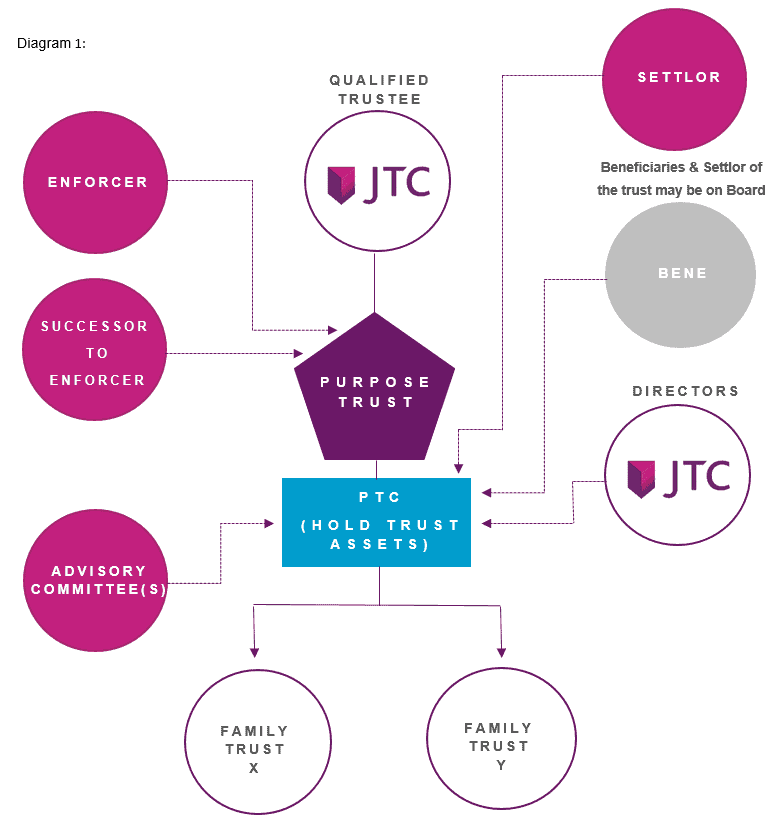

A PTC in its simplest form is a company formed for the specific purpose of acting as trustee of a family trust or a group of the family trusts. This type of vehicle is used to provide trustee services to family businesses similar to those provided by a fiduciary or trustee company. However, the Mauritius PTC does not need to hold a specific fiduciary license so long that it is acting as trustee for a single family trust or a group of related family trusts. In essence, the PTC enables family members including the settlor as director on the Board of the trustee to retain a greater degree of control over the trusts’ affairs without compromising the validity of the trust structure. Such a structure also allows families to select investment managers for specific asset classes. A PTC is legally incorporated as a limited liability company and may apply for a Global Business Corporation (”GBC”) licence (while awaiting clarification from the FSC on whether an authorised company would also be eligible). Below is an example of the use of a PTC in a trust structure, commonly used by wealthy families as part of their estate planning.

A purpose trust is usually set up for the sole purpose of holding shares of the PTC. Since the purpose trust has no beneficiaries, no person has any right of ownership over the shares. It is unlikely that the PTC will be deemed to be owned by an individual or a company thereby avoiding any tax implication and other claims that may otherwise arise. The purpose trust must be administered by a qualified trustee like for instance, JTC (Mauritius).

The PTC is then incorporated to act as trustee for family trusts as above.

Family trust X and Y and/or other connected trust/s may each own different types of assets such as non-income producing assets, for instance, real estate, yachts, planes and also charitable trusts. The assets of the family trusts may alternatively be held by a holding company set up one tier under the PTC and managed by its board. As mentioned above, to avoid carrying out a licensable fiduciary activity, the PTC should act as trustee solely to a limited number of related family trusts, either for the benefit of a single family or for the benefit of different branches of a family or distinct but related family groups. The administration, investment management services or investment advice required in connection with the family trusts are contracted out by the PTC under a service agreement to licensed financial institutions or service providers. It is also to be noted that different structures may be used whereby the PTC may be established as a Company without share capital (company limited by guarantee) to own Special Purpose Vehicles (SPVs) for financing purposes.

Case Study: Use Of PTC Structure

Mr. Mahendra Patil was born in 1941 in Jaipur, India. He got married to Sumitra Jaydev in 1966. The couple has three sons, Mahesh, Sudesh and Dinesh, born in 1969, 1972 and 1975 respectively. In the 1980s after having completed his MBA, Mr. Mahendra along with his family joined the tide of Indians migrating to Nairobi in search of better prospects for himself and his family. During his lifetime, Mr. Mahendra has established three lines of business, namely, seed production, real estate and hospitality. He is the sole owner of three companies under the name of Patil Seeds Ltd (“PSL”), Patil Real Estate Investment Ltd (“PREIC”) in UK and Patil Hotels Resort Ltd (“PHRL”) respectively. Mahendra Patil is now 72 years old and is also one of the non-executive directors on the Board of the three companies. His elder son, Mahesh is resident in Tanzania. He holds an Msc in Agricultural Engineering from Sokoine University of Agriculture, and is the managing director of PSL. Mahesh got married to Sonia and has two children. Sudesh holds a post graduate degree in Finance from the University of Heriot-Watt and is a director of PREIC. He got married to Deena Ramdass in 1998 and has two children, Danny and Wendy. Dinesh has completed his MSc in Hospitality & Tourism Management from Kenyatta University in 1997. Dinesh is the executive director of PHRL in Kenya. He is married to Ria and they have three children.

Mr Mahendra is now a resident of Switzerland where he had moved two years ago for better medical treatment following diagnosis of a major health problem. He has approached JTC to set up a trust structure for estate planning purposes. As he is rather conservative, he wishes to retain some control over his affairs during his lifetime and also wants to involve his sons in the management of the trust structure. He also wishes that three separate trusts be set up to hold the three companies distinctly for the benefit of each of his sons and their families.

JTC has proposed to Mr Mahendra the above structure and the setting up of three separate trusts, the PTC and one purpose trust. The PTC will apply for a GBC licence in Mauritius and will have to appoint two Mauritius resident directors in addition to Mr Mahendra and his three sons (who wish to be involved in the management of the trust structure). At least one physical board meeting will be held in Mauritius per annum.

Taxation

The PTC is taxed like a GBC company but given that it will not be receiving distributions from the trust it will not have any taxable income. The PTC may charge professional or trustee fees to the trusts to cover its own running costs. The trusts including the purpose trust may elect to be a non-tax resident in Mauritius.

Costs & Timeline

The formation and annual maintenance costs for the PTC will be as per the standard fees for a GBC company (see annexed) and the formation and annual trustee fee for the trusts will be as per the standard fees for the trusts (see annexed). The GBC will have to comply with the prevailing enhanced substance requirement applicable such as employing directly or indirectly one staff in Mauritius and incurring a minimum annual expenditure of USD 15,000 in Mauritius. The purpose trust will have as additional costs the fees payable to the enforcer and the successor to the enforcer. Audited account will have to be prepared in Mauritius for the PTC and hence, it will need to have an auditor. It may take 20-30 business days to form a PTC and two days for the set-up of a trust subject to receiving all the necessary documentations on the principles involved in the structure.

Stay Connected

Stay up to date with expert insights, latest updates and exclusive content.

Discover more

Stay informed with JTC’s latest news, reports, thought leadership, and industry insights.

Let’s Bring Your Vision to Life

From 2,500 employee owners to 14,000+ clients, our journey is marked by stability and success.