Bouncebackability: A Game of Two Halves

With European private equity having started the year on rather uncertain ground, James Tracey looks at recent figures to explore what trends are on the horizon and suggests that, as we approach 2020, the outlook for the industry is looking far more positive…

The story so far

There’s no doubt that, particularly in the middle market, European private equity has been extremely competitive throughout 2019, with the result that fundraising and new fund launches have been, generally speaking, underwhelming.

However, as we come closer to the end of 2019, the future is looking much brighter, with European private equity deal value soaring in the third quarter of the year to €122.7 billion, representing a 24.8% uptick quarter-on-quarter, according to figures from PitchBook (‘European PE Breakdown, Q3 2019’).

The industry has bounced back considerably in the latter half of the year, with this bolstered deal value standing in stark contrast to the rocky start for European private equity at the beginning of 2019, when we witnessed a large decline following a record showing in terms of deal value in 2018.

In addition to this deal value growth, the same figures also point to an acceleration in capital commitments for private equity growth funds, with PitchBook even hinting that we could be on track for “a record year”.

Not only that, but European private equity fundraising is also “on track” to hit the third-highest annual level on record with €51.6 billion raised across 64 funds.

It really has been a game of two halves this year, and this all chimes with what we are seeing at JTC too, with a healthy amount of private equity enquiries converted in 2019 and more in the pipeline.

Nevertheless, there are a number of key issues on the horizon too, that managers and investors will need to keep close to if we are to maintain this momentum.

The ‘B’ word

Unsurprisingly, there’s been considerable focus on what Brexit might mean for private equity in the UK this year.

If there’s one word that has tended to define the environment in 2019, it is ‘uncertainty’ – but, despite concerns surrounding Brexit and ‘uncertainty’ in the UK, deal volume in the UK and Ireland has actually remained fairly resilient, according to PitchBook figures.

Whilst all European regions experienced declines in private equity deal volume quarter-on-quarter, the UK and Ireland posted the second-smallest decline (-12.5%).

Of course, it’s inevitable that Brexit would have an impact on the European landscape at large, but the fact that the macroeconomic headwinds associated with it, and which were predicted to affect the UK in particular, have had a much smaller impact on the UK than they have on most other European regions is a really positive reflection of the strength and optimism in the UK market.

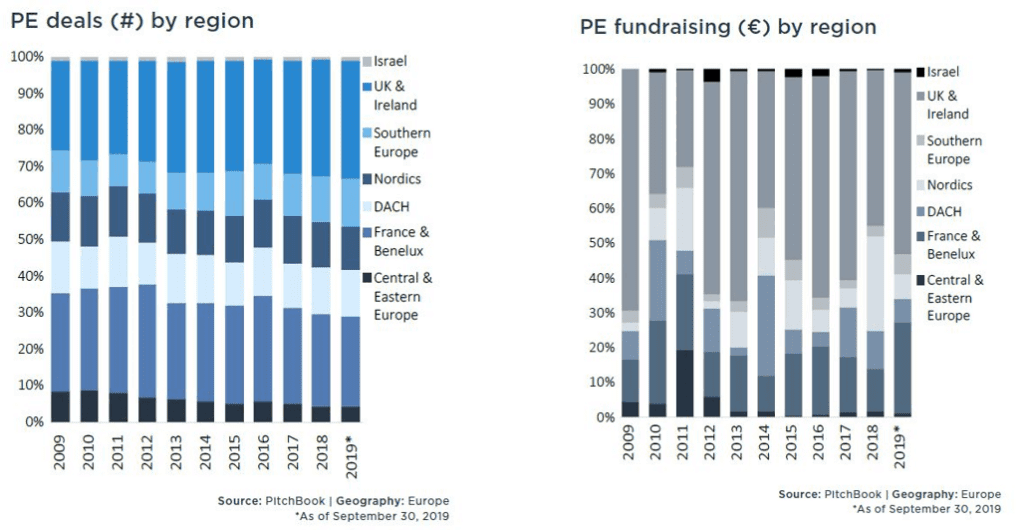

As the above tables show, the UK and Ireland are still at the forefront for the number of private equity deals and fundraising value by region.

As we move forward into 2020, the clear indications are that, despite the impact of Brexit, the UK and Ireland is still a market-leading region in the context of Europe, and should absolutely not be overlooked. Indeed, the region looks set to be a key driver in the European private equity landscape over the coming twelve months.

ESG: Striking forward with purpose

One of the key themes to emerge in the private equity landscape – not just in Europe but more widely too – has been Environmental, Social and Corporate Governance (‘ESG’) investing, as investors have sought increasingly to rise to the challenge of tackling key global environmental and social issues.

ESG has been a particularly hot-topic in 2019 and the expectation is that it will become increasingly important in 2020.

PitchBook figures, for example, suggest that long-term private equity funds and ESG funds will continue to proliferate in the marketplace with ESG funds having strong growth prospects in 2020. This is backed up by Preqin, who found that almost 50% of investors have turned down a fund that did not comply with their ESG strategy (‘Preqin Investor Update: Alternative Assets H2 2019’).

Both PitchBook’s and Preqin’s findings make it absolutely clear that companies will need a defined strategy for ESG in 2020 if they want to be at the forefront of the marketplace.

At JTC, we understand the importance of ESG risks and opportunities for international asset managers and the detailed work that is required to appropriately consider and address such risks and opportunities as part of a wider approach to corporate responsibility.

Looking ahead, we would fully expect further sophistication in the ESG sector as investors look for enhanced core reporting and benchmarking to enable them to demonstrate their commitment to ESG as part of their holistic strategies. As an administrator with deep expertise across a range of asset classes, this is an area we will continue to focus on as we look to support clients in delivering their ESG commitments.

Likewise, we are committed to our own ESG policies and in particular to equal opportunities and wellbeing for our global workforce and comprehensive governance and compliance practices.

Conclusion

The path ahead is by no means easy, but with fundraising and deal values markedly on the up in the second half of the year so far according to PitchBook’s figures, the European private equity industry has shown remarkable ‘bouncebackability’ and that should be a real source of reassurance for managers.

Key to maintaining that trajectory will be staying alive to the key drivers in the sector, in particular the impact of Brexit and the relative strength of the UK compared to other European regions for deals and fundraising, and the rapid rise and increasing sophistication of ESG investing.

From a JTC perspective, we will continue to be focused on providing a multi-jurisdictional platform that is entirely geared up to responding positively to these trends and that can enable managers to meet their objectives over the year ahead. We understand that our clients need not only demonstrate their own ESG credentials, but also that they partner with service providers that share the same fundamental values.

To download a PDF version of this article please click on the download button below.

Stay Connected

Stay up to date with expert insights, latest updates and exclusive content.

Discover more

Stay informed with JTC’s latest news, reports, thought leadership, and industry insights.

Let’s Bring Your Vision to Life

From 2,500 employee owners to 14,000+ clients, our journey is marked by stability and success.