Employer Solutions Insights: Am I Saving Enough for Retirement?

Thinking about retirement is not something many people tend to do when they are in the early stages of their career, and the most common response to the question “Am I saving enough for retirement?” tends to be “I have no idea”.

There are a number of reasons why people may not ask themselves that question – perhaps because pensions are boring, thinking so far ahead is scary, retirement is perceived to be too far away, or they genuinely do not have any interest in knowing the answer.

If this sounds familiar, then you are not alone – however, as any financial adviser will tell you, it is a question that everyone should ask themselves sooner rather than later.

The truth is, whilst it is never too late to start contributing to a pension, the earlier you start saving, the easier it will be to achieve your target.

There is good news too – there are various tools available to help ascertain what an appropriate level of saving is for a desired lifestyle or pot size at retirement.

It really all depends on what sort of lifestyle you expect to have once you finish working, what sort of contributions you can make personally to a pension pot on a regular basis, and whether there is a company pension scheme in place too.

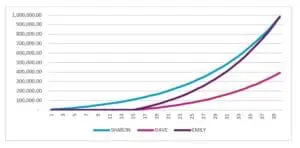

Consider the following examples:

- Sharon starts saving for her retirement aged 25. She contributes 4% from her salary each year and her employer has a generous matching arrangement which increases her 4% employer contribution by another 4%. By starting to save early, Sharon’s eventual retirement pot is worth almost $1m.

- Sharon’s co-worker Dave earns the same as Sharon. He saves at the same rate as Sharon but waits until he is 40 – 15 years later than Sharon. Dave’s eventual retirement pot is less than $400k.

- Another co-worker, Emily, has also waited until she is 40 before she starts saving. She sees that Sharon has amassed a sizeable retirement pot and starts saving to match Sharon. Emily has to save 30% (22% from her salary plus 8% from her company) to reach the same retirement pot size as Sharon.

This graph* illustrates the different outcomes based on those examples. If there is one key takeaway from this, it should be that thinking sooner rather than later about putting money aside on a regular basis is certainly to be encouraged.

In fact there is evidence that younger generations are starting to think about this more – the recently published Transamerica Retirement Survey, for instance, found that with each generation in the US, people are starting to save for their retirement sooner. It revealed that Generation Z, the youngest generation the survey included, started saving for retirement on average at 19. In comparison, millennials started saving at 25, Generation X at 30, and baby boomers at 35.

This is a welcome trend and good news for younger people, especially when considering the above retirement pot illustration.

*This graph is hypothetical and there are a number of market factors that could impact retirement savings. Individuals should seek out independent financial advice and this is not to be construed as providing financial advice.

Key contact

Stay Connected

Stay up to date with expert insights, latest updates and exclusive content.

Discover more

Stay informed with JTC’s latest news, reports, thought leadership, and industry insights.

Let’s Bring Your Vision to Life

From 2,500 employee owners to 14,000+ clients, our journey is marked by stability and success.