The Rise of Co-Investments

What has led to the rise in co-investments, and are they here to stay?

In recent years, the trend of co-investing has gained increased traction as General Partners (GPs) continually innovate mechanisms to secure capital while Limited Partners (LPs) endeavor to optimize returns and attenuate fees. The increased cost of debt has also contributed to the popularity. GPs are looking to structure deals with less leverage that they have previously been able to in a low interest environment and therefore seek larger equity contributions to fund buyouts. LPs provide a friendly source of capital when presented with co-investment opportunities.

These strategies remain a noteworthy consideration for both GPs and LPs in 2024, given their distinctive potential advantages and the unique attributes that lend themselves to the current fundraising market.

The benefits of co-investing for LPs encapsulate several key aspects:

- Direct Access and Exposure Management: Traditional fund-of-funds vehicles distribute investments across numerous portfolio entities; co-investment practices provide a contrast to this approach. LPs gain the opportunity for more direct returns from specific portfolio companies. This strategy, deployed in concurrence with various GPs, adequately preserves diversification while allowing the LP greater control in crafting their portfolio to regulate levels of exposure to certain sectors.

- Fee Reduction: With increasing pressure on minimizing fees, co-investment serves as a strategy to maintain equity investment levels without the corresponding fee burden typical of a conventional private equity fund.

- Pace of Deployment: Conventional co-mingled private equity vehicles often involve an extended capital deployment timeline over several years. Co-investment provides LPs with the capability to control their capital deployment, somewhat mitigating the heightened prominence of the J-curve effect in recent time times.

- Due Diligence Accessibility: Co-investment vehicles offer LPs an opportunity to evaluate GPs’ investment processes, affording them greater control and transparency not typically afforded in traditional arrangements. Such proximity offers potential benefits to GPs as well, as further detailed below.

There are also significant benefits for GPs, including:

- Capital Access: By diversifying offerings beyond traditional mechanisms, GPs can sustain capital levels, despite the current fundraising challenges across the industry.

- Fundraising Pace: Preqin data indicates that the average fundraising duration for a co-investment fund is approximately eight months, significantly less than the average 22-month period for private equity overall1.

- Relationship Cultivation: Facilitating select LPs with exclusive investment opportunities and insight into the GPs’ internal processes can foster deeper relationships, enhancing the probability of continued investment in subsequent capital raises.

This strategy, nevertheless, is not devoid of its own challenges, necessitating the establishment of clear relationship parameters from the outset. For example, while some LPs may prefer a relatively passive stance, others might seize co-investment as an opportunity for enhanced influence. For GPs, the potential for relationship development with co-investing LPs exists, but at the risk of potentially alienating other LPs who might perceive this as favoritism and offering an unfair advantage.

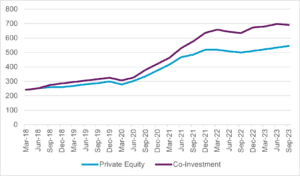

In addition, co-investments continue to outperform investments into traditional private equity structures on a global basis, as demonstrated by Preqin’s quarterly index return data, shown below.

Source: Preqin.

Over the last 10 years there has also been an increase in the number of co-investment funds fundraising. From 2014 this figure stood at 77, compared to 342 in 20212.

Capitalizing on relationships

In terms of the future of co-investments, despite increasing LP demands, there are many reasons to anticipate continued growth over 2024 and 2025. As well as persistent fundraising challenges and co-investment funds continuing to demonstrate higher returns, the much-discussed democratization of private equity could also influence this trend. As the private capital sector becomes increasingly inclusive, LPs are going to be looking for ways to capitalize on their long-standing relationships and experience in the market. One approach could be to channel their deep-seeded GP relationships though co-investing in bespoke deals through co-investments. Moreover, the increased demands and technological requirements faced by private equity managers, combined with higher liquidity needed to lure the retail capital market could also threaten to increase management fees associated with traditional funds, providing more of a reason to explore further co-investment opportunities for LPs.

Focus on control

The associated legal frameworks and governing prerequisites of a co-investment structure typically share many similarities with traditional private equity funds. However, the intimate nature may demand more initial negotiations. For example, with the rise in popularity of GP-led secondaries and continuation vehicles, LPs have started to focus on the GPs’ ability to convert their co-investment into a continuation vehicle. As co-investments inherently require GPs to relinquish a degree of control, additional considerations such as having a say in whether the fund can transition to a continuation vehicle should be anticipated, even if it doesn’t align with the GPs traditional practice of handling their co-mingled vehicles.

To find out more, please get in touch with Dewi directly or visit our dedicated US webpage.

1Preqin data.

2Preqin data.

Key contact

Stay Connected

Stay up to date with expert insights, latest updates and exclusive content.

Discover more

Stay informed with JTC’s latest news, reports, thought leadership, and industry insights.

Let’s Bring Your Vision to Life

From 2,500 employee owners to 14,000+ clients, our journey is marked by stability and success.