Inflation in 2023: Stealing returns as you sleep

“Inflation is not only unnecessary for economic growth. As long as it exists, it is the enemy of economic growth” Henry Hazlitt, author of Economics in One Lesson.

At its most basic level, inflation can have a significant negative impact on cash held in a standard bank account as it erodes the purchasing power of cash over time, meaning that the same amount of money will have less buying power in the future than it has today.

Inflation vs interest

After a period of low inflation and interest rates globally, companies, individuals and the general public are having to come to terms with rising inflation with lagging interest rates comparably.

One of the main reasons inflation can have such a negative impact on cash is that a low interest rate paid on a standard bank account is usually not high enough to keep pace with inflation. In fact, the interest rate paid on these accounts is significantly lower than the rate of inflation, meaning that the real value of the money in the account can decrease substantially over time.

The Bank of England’s inflation calculator demonstrates how prices in the UK have changed. The following graphic shows how since 2008 to now goods and services cost over 50% more:

An interesting way to look how inflation and interest affects us is captured in the following example: You have £1,000 in a bank account that is paying 0% interest. If the rate of inflation is c.10%, then in one year’s time, the real value of your £1,000 will have decreased to c.£900. In other words, even though you still have £1,000 in your account, the purchasing power of that money has decreased by approximately 10%.

Compounding the inflation, most institutional bank accounts charge fees which can further erode the value of your cash over time. For example, if your bank charges a monthly account maintenance fee of £50, then in one year’s time, your account balance will have decreased to £900 – £600 (12 months x £50) = £300.

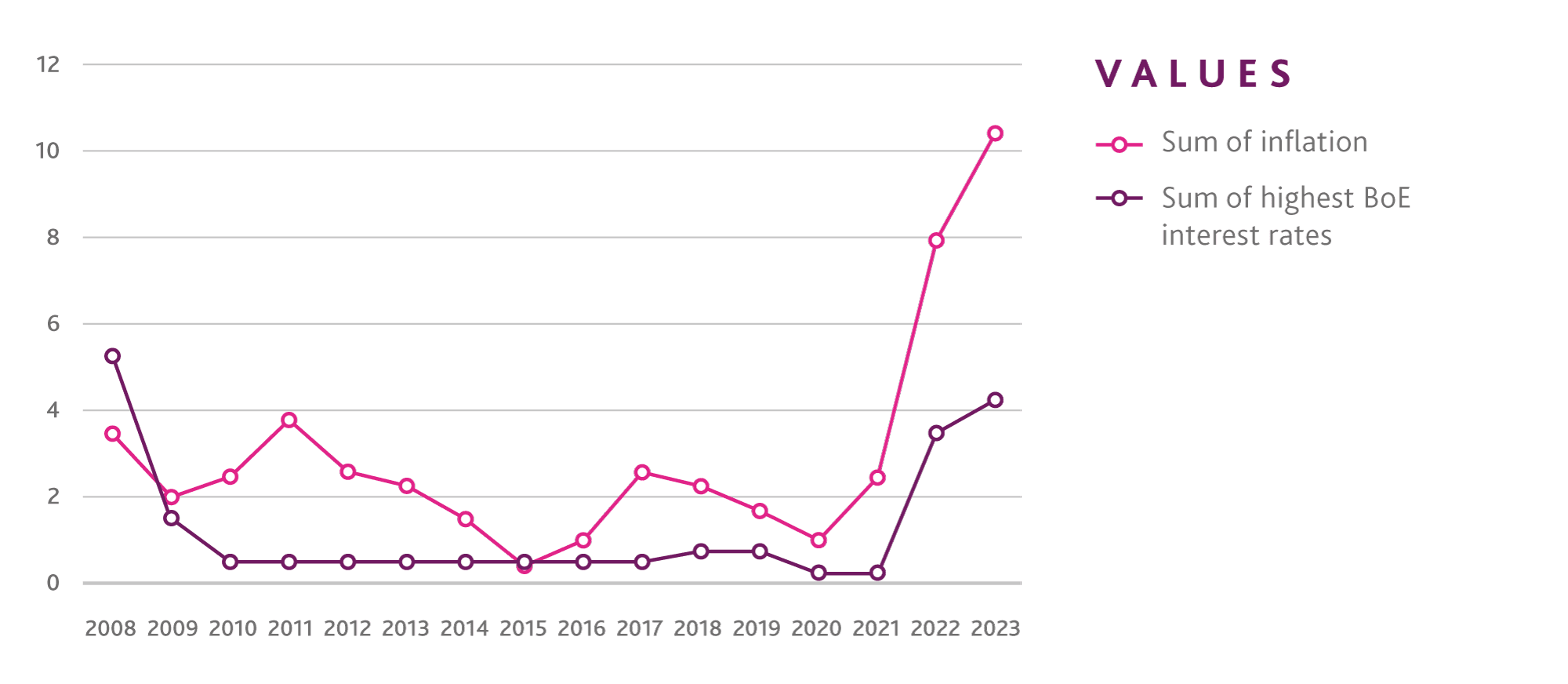

The below graph shows the gap between inflation and interest rates which highlights the importance of making your cash work effectively (Source: Bank of England):

How can you protect your cash in a time of rising inflation?

One option is to diversify funds over multiple banks. By spreading cash across several different banks, the risk of losing all your money if one bank fails can be replaced. This is especially important in times of banking uncertainty, such as the global financial crisis in 2008 or the recent demise of SVB and Signature in the US.

From a risk mitigation viewpoint, having multiple bank accounts can be beneficial. However, it is important to note that running multiple bank accounts can also be costly to administer and can incur multiple bank charges. Fees may have to be paid to open and maintain each account, and it can be time-consuming to keep track of all accounts and balances.

It is important to find the best solutions for cash in high inflation environments. This may involve researching different banks and their interest rates, as well as exploring alternative cash products, such as fixed deposits. This can be a time-consuming and resource intensive task.

It is also worth noting that while most standard bank accounts are paying very low levels interest, some banks offer higher interest rates on their accounts but only to institutional investors. These rates can help to mitigate the negative impact of inflation on your cash but are not usually available to all.

Ultimately, the key to protecting cash from the negative impact of inflation is to be proactive, keep informed and stay agile. If you do not have the time to keep on top of inflation and interest rates, and the willingness to explore different cash products and banks to find the best solutions for your needs, the best option could be an outsourced provider allowing you to focus on core business goals.

JTC Banking and Treasury

Our team have over 205 years’ collective experience, trusted to look after circa. £1.5 billion of clients cash with a proven track record of providing treasury services to our clients for over 15 years.

We work with a number of carefully selected banks to provide our clients with a range of cash management solutions. These solutions allow clients to take advantage of some or all of the following benefits:

- Better rates – Better interest rates than generally offered on comparable banking arrangements

- More security – Diversification of bank risk, without the cost of maintaining multiple bank relationships

- Extra options – No-notice access to money held on deposit and bespoke solutions

There are compelling arguments for diversifying bank risk; however opening and maintaining multiple banking relationships is expensive, and satisfying banks’ increasingly complex due diligence requirements time consuming. JTC’s Diversified Treasury Account overcomes this by combining clients’ monies into a dedicated JTC client pool which is then apportioned across a carefully selected range of banking institutions.

If you would like to learn more about our banking and treasury solutions please contact Paul Fosse, Group Head of Banking & Treasury.

Stay Connected

Stay up to date with expert insights, latest updates and exclusive content.

Discover more

Stay informed with JTC’s latest news, reports, thought leadership, and industry insights.

Let’s Bring Your Vision to Life

From 2,500 employee owners to 14,000+ clients, our journey is marked by stability and success.