ESG in the Investment Trust Industry 2024

Environmental, Social & Governance (ESG) and sustainability issues are becoming increasingly important for investors. Due to the ever-evolving variety of ESG frameworks and standards, the regulatory landscape is becoming increasingly difficult to navigate.

JTC has conducted research to pose the question of which ESG frameworks and standards are being adopted in the greatest numbers – and by whom. This study also endeavours to identify some key themes and trends within the investment trust space.

The research spans 375 investment trust companies across 52 sectors belonging to the Association of Investment Companies (AIC).

To discuss the findings, learn more about JTC’s Sustainability Services, or discover the ESG journey that JTC Group continues to undertake, contact David Vieira, Gregory Yianni or Jon Masters directly.

You can download the full whitepaper here or read online below:

Table of Contents

- Executive Summary

- Foreword by the Association of Investment Companies (AIC)

- Sectors in Scope

- Methodology

- Key Findings

- Conclusion

- Glossary

- Acknowledgements

Executive Summary

Environmental, Social & Governance (ESG) issues are becoming increasingly important for investors. Due to the ever-evolving variety of ESG frameworks and standards, the regulatory landscape is becoming increasingly difficult to navigate. Between March and July 2023, JTC conducted research to pose the question of which ESG frameworks and standards are being adopted in the greatest numbers – and by whom. This study also endeavours to identify some key themes and trends within the investment trust space.

The research spans 375 investment trust companies across 52 sectors belonging to the Association of Investment Companies (AIC). The companies included in this research are primarily registered in the British Isles, though nine other regions are represented to varying degrees. Data was collected at the company level. This data includes basic contextual information about each investment trust, as well as ESG policy-specific data.

The data indicates a varying level of adoption, perhaps in part due to the relevance of the framework or standard to the sector the investment trust company operates in. The mean number of ESG standards adopted across all companies is 1.5. The most commonly adopted framework is the United Nations Principles for Responsible Investment (UNPRI), with 78% of companies (or parent companies) being a signatory. The Task Force on Climate-Related Financial Disclosures (TCFD) and the United Nations Sustainable Development Goals (UNSDGs) were the second (23%) and third (15%) highest adopted frameworks respectively.

The adoption of standards varies between sectors, with some being clear frontrunners (such as Renewable Energy Infrastructure, Infrastructure, Private Equity and UK Property sectors). The dataset suggests that larger companies tend to adopt a greater number of ESG standards, with FTSE 250 companies adopting an average 2.1 standards, compared to an average of 1.2 standards adopted for other companies in the dataset. Generally, ESG reports across the 375 companies are short, approximately seven pages, with many dedicating a page or less to ESG issues.

Most of the ESG frameworks and standards included in the research are voluntary, or are voluntary for most companies. Adopting ESG frameworks and standards has associated costs, but also provides an opportunity for an investment trust company to differentiate itself in a market that is becoming increasingly ESG conscious. Can an investment trust company really afford not to address ESG issues in a regulatory landscape that is steadily moving from ‘voluntary’ to ‘mandatory’?

Foreword by the Association of Investment Companies (AIC)

ESG reporting is at a crossroads. The Financial Conduct Authority’s (FCA) publication of its Sustainability Disclosure Requirements (SDR), along with its four planned investment labels, heralds a shift towards a more rules-based system.

This is not before time. We know from the AIC’s own ESG Attitudes Tracker that less than 1% of financial advisers and wealth managers completely trust sustainability claims from funds. Nearly two-thirds of private investors are concerned about greenwashing[1]. SDR provides the investment industry with an opportunity to get its house in order and win back investors’ confidence.

The ESG standards and frameworks discussed in this report will play an important role in the FCA’s new regime. To qualify for an investment label, for example, at least 70% of a fund’s portfolio must be invested in accordance with the fund’s policy, which must be based on a “robust, evidence-based standard”.

As this report demonstrates, investment trusts have adopted a range of different standards and frameworks for their ESG reporting. The board of every investment trust must make a judgment on which standards or frameworks, if any, are relevant to its strategy. We are a diverse sector investing in everything from mainstream equities to wind farms, from healthcare properties to space technology. Given this diversity it is inevitable that, as the report highlights, the extent to which individual investment trusts highlight ESG issues, adopt specific standards, or promote their ESG credentials will vary significantly.

That said, many investment trusts have strong ESG credentials, and clear labelling and disclosures will enable investors to identify those companies amongst the wide range of investment choices. The ability to invest freely in less liquid assets is one of the benefits of our closed-ended structure. It expands the investment universe, giving investors access to investment opportunities that would otherwise be unavailable. Crucially, this includes assets with positive social or environmental impact, such as renewable energy infrastructure and social enterprises.

ESG reporting is, as the report notes, ever-evolving. Significant progress has been made and it is set to develop rapidly in 2024 as the different elements of SDR and the labelling regime are implemented. This report shines a light on the adoption of ESG standards and frameworks in a pre-SDR world, and provides a useful baseline for monitoring future progress. Investment trusts have the scope to offer investors real differentiated opportunities. The evolution of reporting, where relevant to individual investment trusts, will enable investors to better identify those opportunities that resonate with their own values and objectives.

Richard Stone

Chief Executive of the Association of Investment Companies (AIC)

[1] https://www.theaic.co.uk/aic/news/press-releases/esg-investing-declining-in-popularity-as-fears-of-greenwashing-grow

Sectors in Scope

Methodology

Between March and July 2023, JTC reviewed public information for 375 investment trust companies – including websites, ESG policies, annual reports (and where applicable, ESG reports) to determine the frameworks and standards that each company had adopted. A database containing this information, along with important contextual information about each trust (for example Market Cap, Date Launched, Management Group etc.) was created and the data within this analysed to determine if there were any key trends.

DATA COLLECTED

The following frameworks and standards were included in the research:

Key Findings

UNPRI is the most adopted standard

UNPRI has the highest adoption rate (78% of the total AIC universe), though it should be noted that this may be due to a parent company/management group of a trust being a UNPRI signatory. This is included in the dataset, as the signatory status should extend to subsidiaries.

TCFD has the second highest adoption rate (23%), and this is the only other standard to have an adoption rate of more than 20%. Investment trust companies are largely exempt from TCFD reporting requirements, as only companies with more than 500 employees are required to comply. Therefore, investment trust companies largely make an active choice to report in line with TCFD guidelines, potentially to appeal to current and future investors.

UNSDGs are included in the ESG policies of 15% of the investment trust companies researched. The adoption of UNSDGs is voluntary and measurement against progress toward the adopted SDG is not prescriptive. It could be argued that one would expect to see higher levels of adoption due to the comparatively basic requirements of the standard, but it could be countered that the investment trust companies do not adopt UN SDGs due to the lack of relevance to their operations or company size.

SFDR reporting is mandatory for all financial market participants with more than three employees that market products in the EU. A UK equivalent, the SDR, will come into force in the near future, but for now, the relatively low adoption rate of SFDR (14%) may be explained by either the fact that the investment trust companies sampled in the dataset do not meet the employee threshold or that they do not market products in the EU.

GRESB (6%) and the EPRA sBPR (5%) are almost exclusively adopted by investment trust companies in real estate sectors, where they have adoption rates of 51% and 54% respectively within this sub-sector. This is a prime example of adoption of a sector-specific ESG framework or standard. The dataset does not necessarily indicate low levels of uptake of GRESB and the EPRA sBPR, rather that the real estate sector is less represented across the 375 investment trust companies sampled.

SASB has the lowest adoption rate (3%) of the ESG standards sampled, and the rate is low across all sectors. The lower levels of adoption could be attributed to the lack of representation of US companies in the dataset. The majority of SASB reporters are US-based, though the number of companies reporting under SASB is growing.

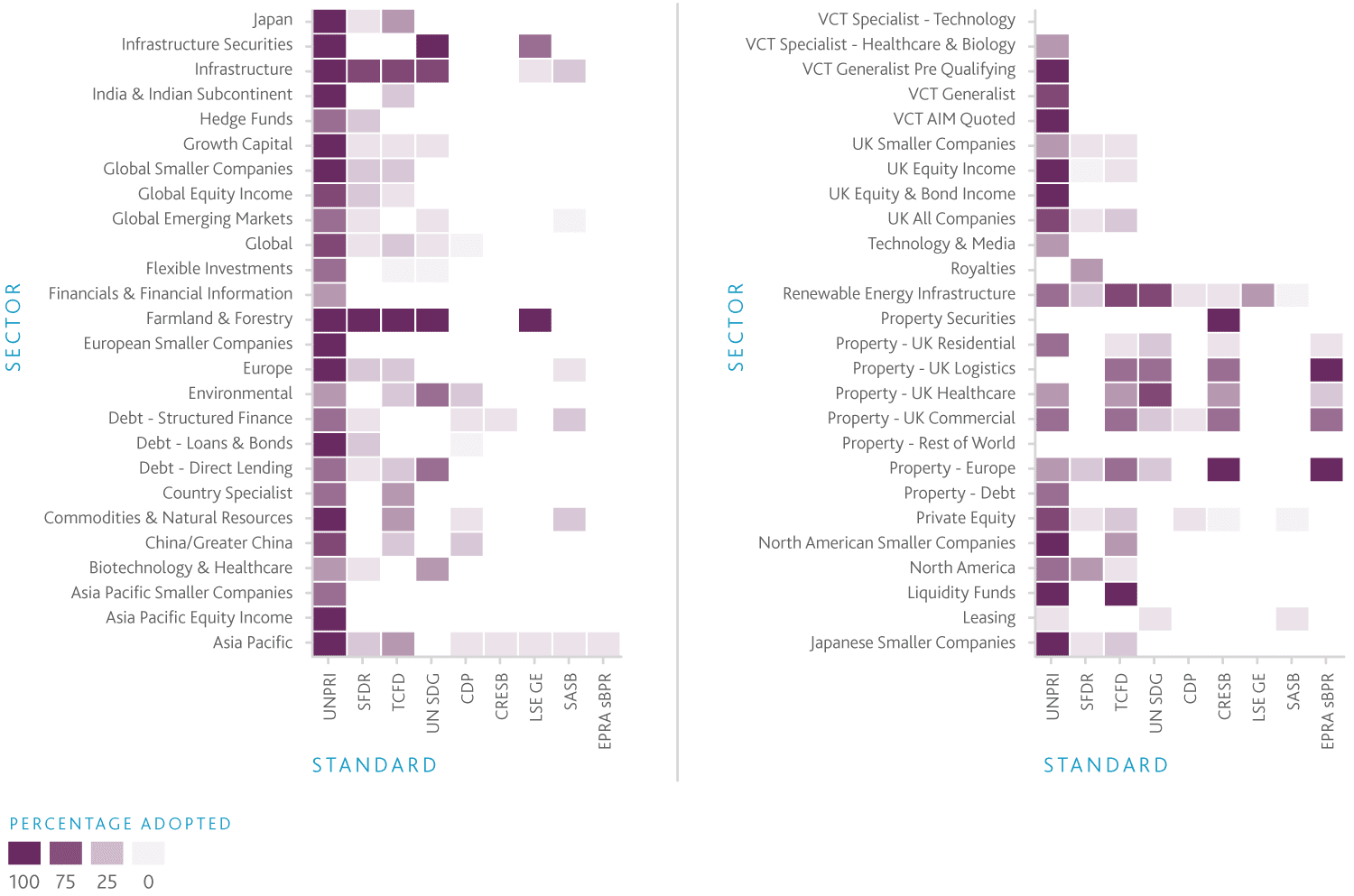

The following heat map shows the large differences in uptake of each of the standards between different sectors. Darker cells indicate a higher adoption rate, while lighter cells a lower adoption rate (with blank cells being zero).

Uptake varies by sector

As seen in the heat map, the sectors adopting the highest number of ESG frameworks and standards are Farmland & Forestry, Renewable Energy Infrastructure, and Infrastructure and Property sectors. Sectors which are comparatively light on adoption of standards include VCT sectors, Financials & Financial Information and Flexible Investments. The relatively high adoption rate of UNPRI is consistent across majority of sectors. There is also a predominance of GRESB and EPRA sBPR in Property sectors. Surprisingly, the ‘Environmental’ sector indicates relatively low levels of adoption of ESG frameworks and standards, though still higher than the majority of the sectors.

There is relatively low level of uptake for SASB and the Global Reporting Initiative (GRI) – the latter has not been included due to significantly low levels compared to the wider dataset. Given their popularity in other regions, higher levels of uptake for SASB and GRI may have been expected. A JTC survey on Opportunity Zones in the US found that uptake levels amongst respondents for SASB and GRI were 31% and 45% respectively. The fact that many investment trust companies fall outside the scope of mandatory regulation is likely a factor in the relatively low adoption rates across the board.

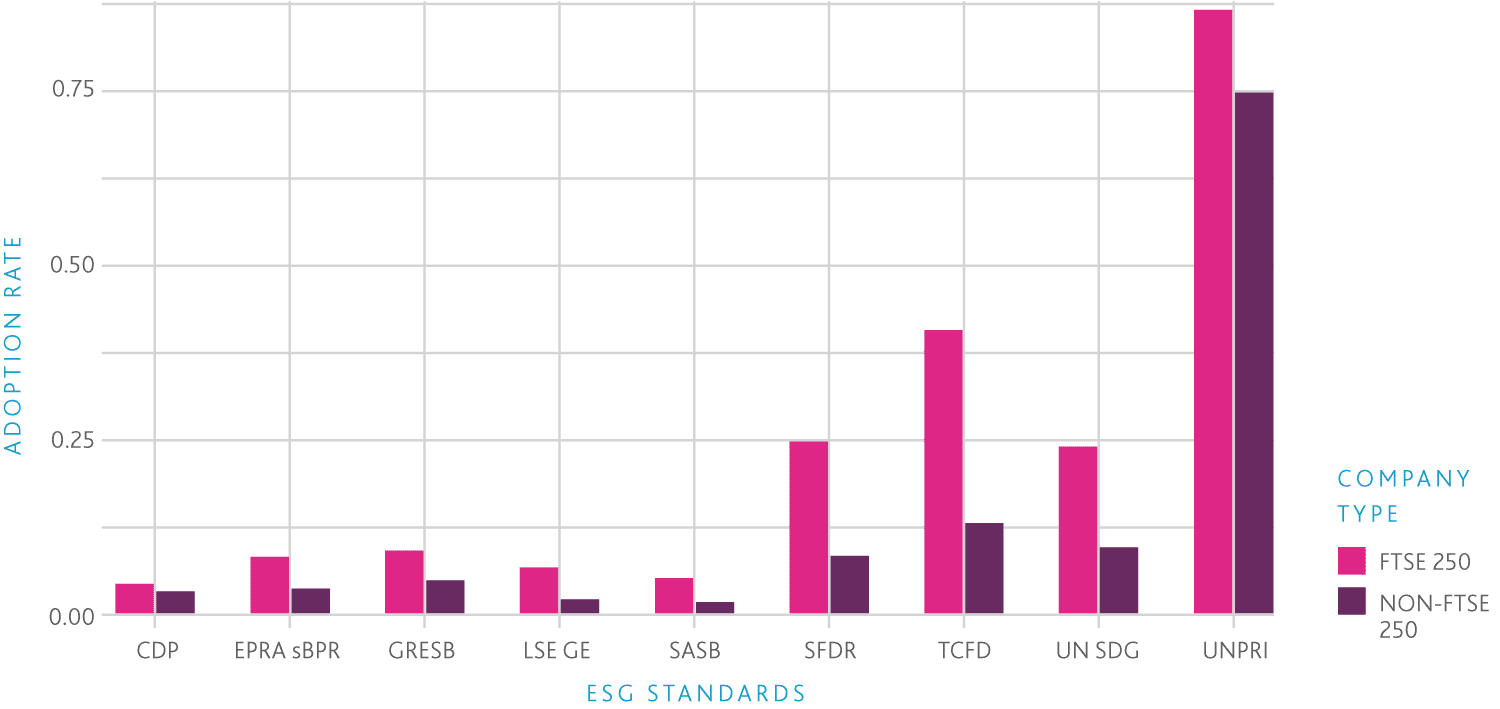

Larger companies generally adopt more ESG frameworks and standards

Of the companies registered with the AIC, 35% are mid to large cap in size and adoption rates are generally higher compared to smaller companies. Adoption rates with the greatest variance between large and small companies can be seen for TCFD (40% vs 13%), SFDR (25% vs 8%) and UNSDGs (24% vs 10%). Research published by the University of Reading seems to corroborate this trend, suggesting that larger companies tend to have more awareness of ESG considerations and ‘twice the chance of using a standard’ compared to smaller companies.

This increased awareness and adoption rate is likely due to the more stringent reporting requirements placed on larger companies. Another reason could be the greater resources at larger companies that would allow for spending (IT infrastructure, staff etc.) to focus on ESG framework adoption, even if it is not mandated.

Nevertheless, the low levels of adoption for UNSDGs is interesting, as this is arguably one of the simpler frameworks to adopt. It is free, has no specific reporting requirements and is not mandated by regulation. There are 17 SDGs; not all of which will typically be applicable, therefore a company has the freedom to choose a sub-set. Interestingly, some investment trust companies included in the dataset decided to adopt all 17 SDGs, raising the question of what meaningful adoption of this framework looks like.

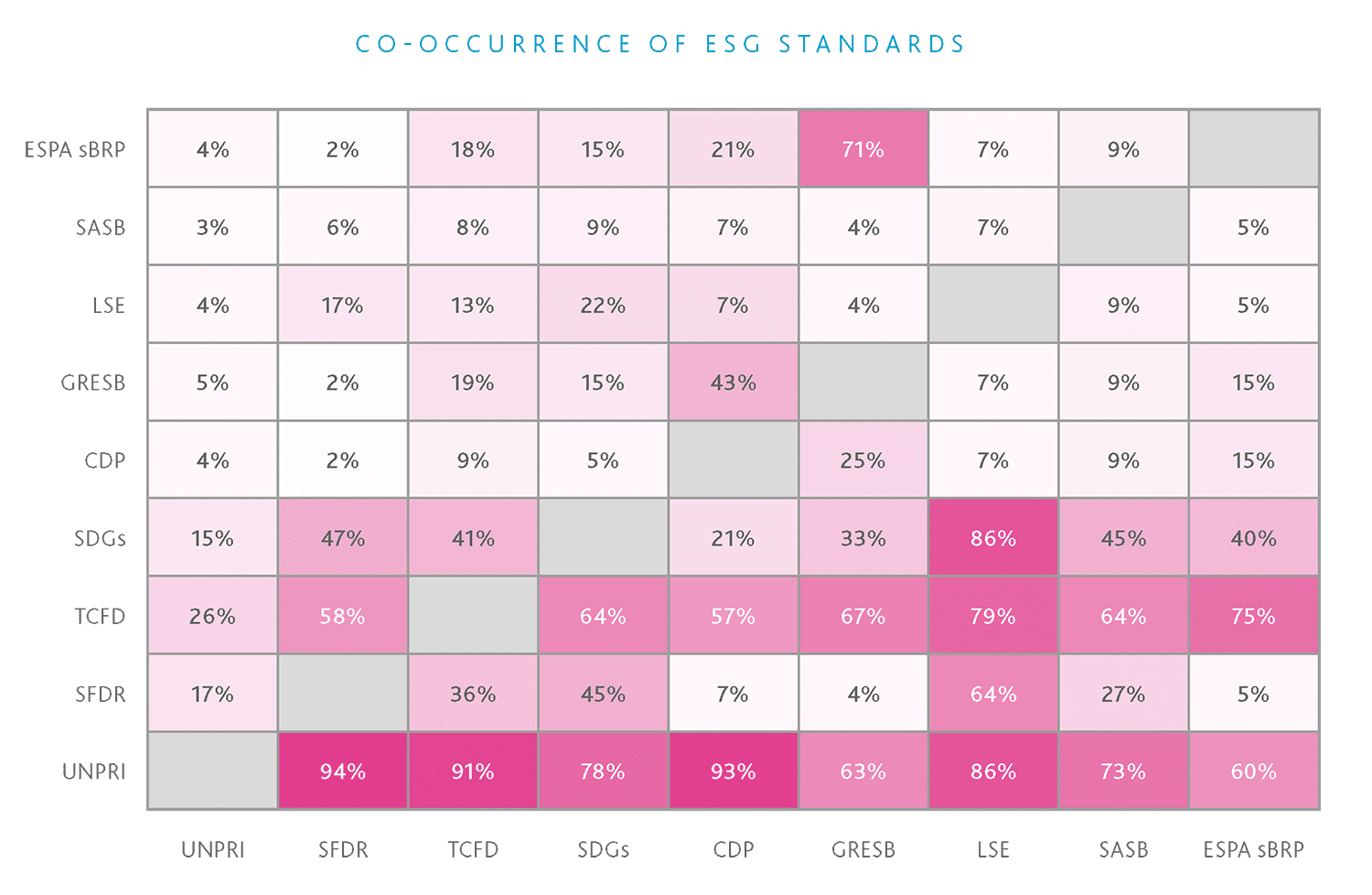

Some standards are adopted together more often

When adopted as the primary framework, UNPRI has a high co-occurrence rate with a number of other ESG standards and frameworks. Notably, 94% of companies that must comply with SFDR have also become UNPRI signatories, indicating a high level of interoperability.

Similarly, TCFD has high levels of co-occurrence with UNPRI at 91%. The real estate frameworks GESB and EPRA sBPR have a predictably high co-occurrence rate, with 85% of companies adopting EPRA sBPR also adopting GRESB, and 71% companies that have adopted GRESB adopting EPRA sBPR.

However, the dataset indicates that co-occurrence with other ESG frameworks or standards is low.

Other ESG frameworks and standards, such as CDP and SASB have fewer common pairings, though it is unclear whether this is due to poor interoperability with other frameworks and standards. It is evident that certain standards are more closely aligned with specific sectors, while others have cross-sectoral relevance. As investment trust companies navigate the new reality of sustainable investing, these co-adoption patterns offer valuable insights for the refinement of ESG strategies.

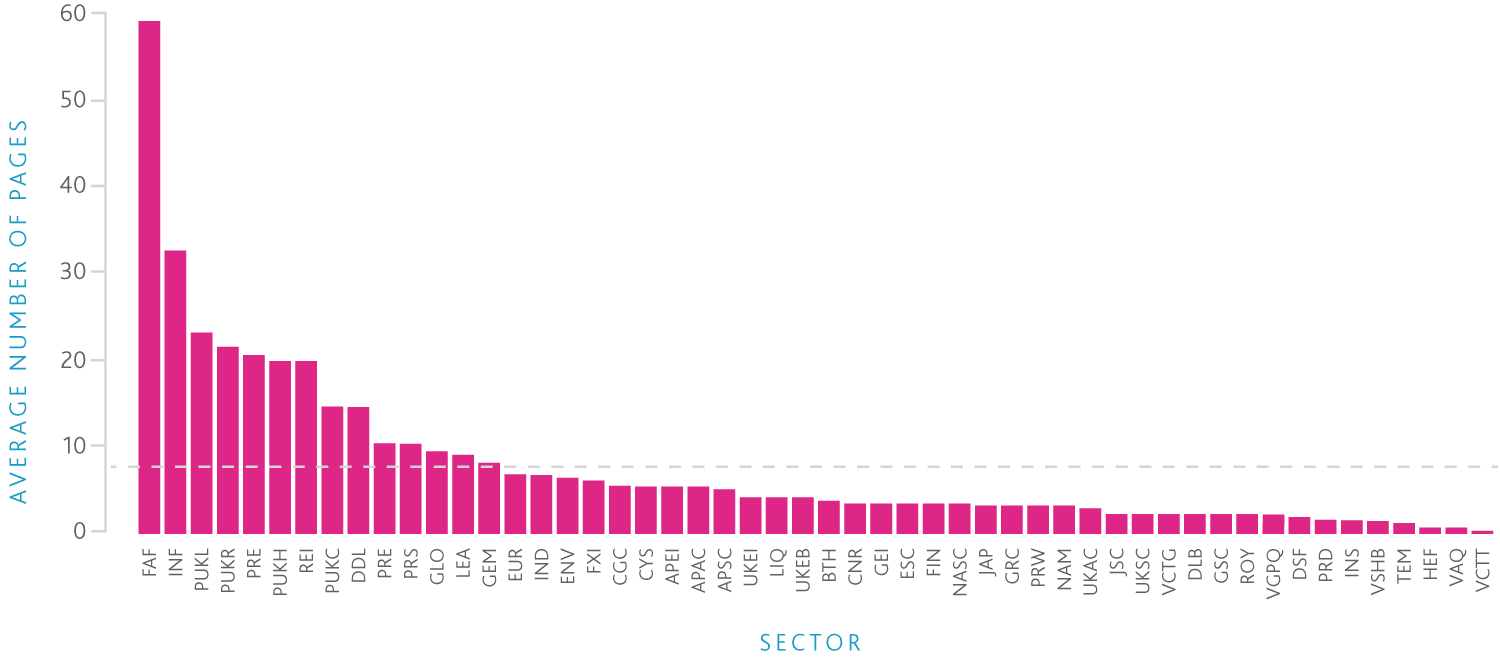

ESG reports are generally short and often lacking details

Annual reports (and dedicated ESG reports) are the key mechanism for communicating the ESG strategy of a trust to investors. Of the 375 investment trust companies sampled, 329 (87%) do not have a dedicated ESG report. This does not necessarily correlate with a lack of adoption of ESG frameworks and standards, as ESG strategy can often be incorporated into broader Annual Reports. Of the 329 investment trust companies that do not have a dedicated ESG report, 291 (88%) do include an ESG section in their Annual Report. Only 10% of the investment trust companies sampled do not provide detail regarding ESG in their publicly available company literature.

The number of pages dedicated to ESG in Annual Reports varies greatly, ranging from half a page to 50. The mean average of pages dedicated to ESG is 6.7, with 8.5% of the dataset dedicating more pages than this. With the increase in attention from investors and the growing ESG awareness of the public, a detailed and dedicated ESG section in an Annual Report provides the opportunity to stand out amongst market competitors.

Some sectors do significantly exceed the average report length, with nine Infrastructure companies boasting ESG reports with an average of 33 pages. Several Property sectors, Private Equity and Renewable Energy Infrastructure sectors also stand out for their comprehensive reporting practices.

It is crucial to highlight that a balance must be found between providing adequate context and falling foul of greenwashing allegations. The most effective ESG reports are those that align with the key aspects of the chosen ESG standards, providing ample detail while remaining concise and relevant. Simply put, an ESG report’s quality is ultimately determined not by its length, but by its content and adherence to adopted standards. By doing so, investment trusts can meet the expectations of increasingly ESG-conscious investors.

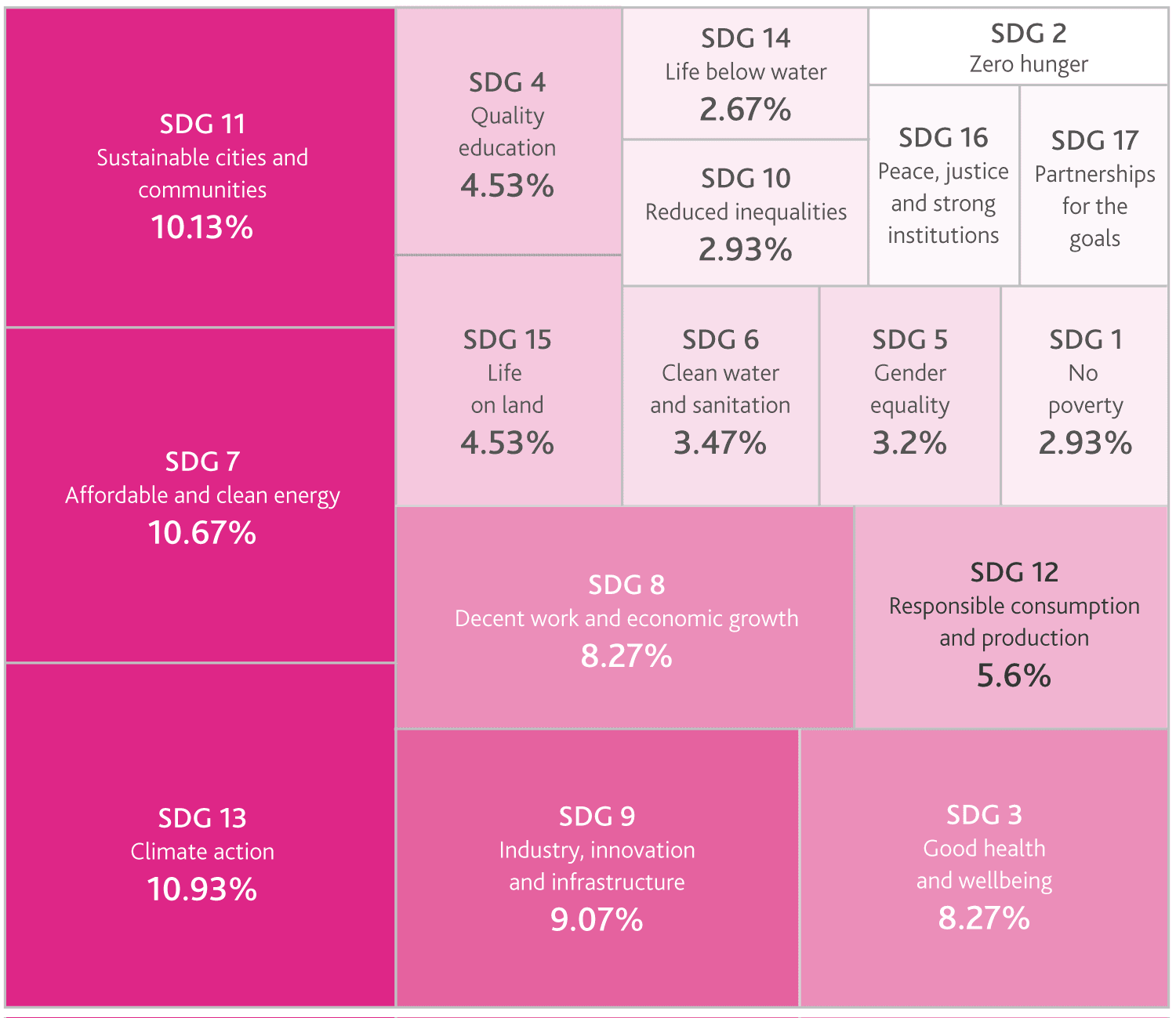

Some SDGs are more popular than others

Of the 375 companies in this research, 55 (15%) have chosen to incorporate UNSDGs into their ESG policies. All 17 SDGs feature at least once, with all companies adopting the SDG most relevant to their sector and business practices.

Among the SDGs, “Climate Action” (SDG 13) and “Affordable and Clean Energy” (SDG 7) have gained the highest adoption rates at approximately 10.9% and 10.7% respectively. This indicates that many companies are recognising the urgency of addressing climate change and supporting renewable energy initiatives. Additionally, “Sustainable Cities and Communities” (SDG 11) and “Industry, Innovation, and Infrastructure” (SDG 9) have also seen reasonable levels of adoption, reflecting what is likely a focus of many trusts on their impact on their local communities.

However, adoption rates for other SDGs, such as “Life on Land” (SDG 15) and “Quality Education” (SDG 4), are lower, with these two seeing adoption rates of 4.5%. Those SDGs with the lowest adoption rates perhaps highlight areas for future growth, but for now, companies do not consider them as relevant to their business strategy. SDGs with more of a focus on ‘Governance’ are less commonly adopted by investment trust companies; those with a ‘Social’ focus tend to be more popular. Overall, adoption rates of SDGs are fairly modest considering the relative ease of choosing to adopt this ESG standard.

Conclusion

- Some sectors within the investment trust space are front runners when it comes to ESG standard adoption

- ESG framework and standard adoption varies between sectors, with an average of ~1.5 standards being adopted by each trust within the AIC

- With the exception of the UNPRI, there is no clear leader for any ESG standard most frequently adopted. The UNPRI has seen a high adoption rate, most likely partially due to the inclusion of this metric when the parent company is a signatory of UNPRI

- Investment companies are largely exempt from reporting requirements, though the most ESG-conscious companies adopt standards such as SFDR and TCFD voluntarily

- The adoption rates of GRESB and EPRA sBPR are high within Property sectors, and these sectors are strong overall

- ESG reports are generally short and undetailed despite investor demand for improvements to ESG reporting

- FTSE 250 companies are generally more likely to adopt a greater number and variety of ESG standards

- UNSDGs that are aligned more with ‘social’ characteristics are relatively popular, though the two most popular are environmental goals for Clean Energy (SDG 7) and Climate Action (SDG 13)

Glossary

Association of Investment Companies (AIC)

The AIC is a trade association that represents investment companies in the United Kingdom. Its members are investment companies and other closed-end funds that invest in a range of assets, including equities, fixed income, property, and alternative investments. The companies researched are all members of the AIC.CDP

CDP (formerly known as the Carbon Disclosure Project)

The CDP is a non-profit organisation that encourages companies and cities to disclose their environmental impacts and strategies for addressing climate change.

European Public Real Estate Association Sustainability Best Practice Recommendations (EPRA sBPR)

EPRA sBPR is a set of voluntary guidelines that provides a standardised framework for reporting sustainability performance in the real estate industry. The guidelines cover a range of ESG issues and promote continuous improvement in sustainability performance by encouraging companies to set targets and track progress over time.

Global Real Estate Sustainability Benchmark (GRESB)

GRESB is an organisation that assesses and benchmarks the sustainability performance of real estate portfolios and infrastructure assets globally. It provides a standardised framework for evaluating the sustainability of buildings and infrastructure.

Global Reporting Initiative (GRI)

GRI is an international independent standards organisation that helps businesses, governments, and other organisations understand and communicate their impacts on issues such as climate change, human rights and corruption.

Sustainability Accounting Standards Board (SASB)

SASB is an independent organisation that provides industry-specific sustainability accounting standards for use by publicly listed companies in disclosing material sustainability issues to investors. By providing a common language for reporting on sustainability issues, SASB aims to improve the quality and comparability of sustainability data.

Sustainable Finance Disclosure Regulation (SFDR)

SFDR is a European Union regulation that requires financial market participants and financial advisors to disclose how they integrate sustainability risks and factors into their investment decision-making processes. One of its purposes is to prevent so-called ‘greenwashing’ by ensuring that companies cannot falsify their ESG credentials. SFDR requires firms to be classified as either Article 6, Article 8 or Article 9:

- Article 6 relates to funds that have no sustainable objective and may include funds that invest in unsustainable products such as coal producers

- Article 8 relates to funds that promote ESG characteristics

- Article 9 relates to funds that have sustainable investment as their objective

SFDR does not apply to all companies as only firms with more than 500 employees and those that are based or market themselves in the EU are obligated to comply, but those with fewer than 500 employees must either comply or explain why they do not.

Task Force on Climate-Related Financial Disclosures (TCFD)

TCFD is a global initiative established by the Financial Stability Board to develop voluntary, consistent climate-related financial risk disclosures for use by companies, banks, and investors. The TCFD framework provides guidance on how companies can disclose climate-related risks and opportunities in their financial filings. TCFD is mandatory for companies with more than 500 employees and a turnover of £500 million+.

United Nations Principles for Responsible Investment (UNPRI)

UNPRI is a global network of investors committed to integrating ESG factors into their investment decision-making processes and ownership practices. The PRI framework provides a set of principles and best practices for investors to follow, which can help them align their investments with sustainable development goals and promote positive social and environmental outcomes. Signing the UNPRI is voluntary.

United Nations Sustainable Development Goals (UNSDGs)

UNSDGs are 17 goals adopted by the United Nations General Assembly in 2015 to address global challenges such as poverty, inequality, climate change, and environmental degradation by 2030. The SDGs provide a framework for governments, businesses, and civil society to work together on sustainability issues. There are many other ESG standards, though these are the most common among the investment companies researched. Additionally, when reference is made to an ESG ‘standard’, it is generally referring to one or all of these.

Acknowledgements

JTC Group would like to thank Oliver Prew for his hard work in compiling and analysing the dataset used in this study.

Key contact

Stay Connected

Stay up to date with expert insights, latest updates and exclusive content.

Discover more

Stay informed with JTC’s latest news, reports, thought leadership, and industry insights.

Let’s Bring Your Vision to Life

From 2,500 employee owners to 14,000+ clients, our journey is marked by stability and success.