US Managers Eyeing European Capital

A fundraising dry spell has led to a flood of US private capital firms targeting European investors, a number of whom are looking to ramp up their exposures to illiquid assets. Nonetheless, it is essential for US managers to thoroughly contemplate numerous factors prior to stepping across the pond to ensure they fully leverage and optimize this significant opportunity.

You can download the full article here or read online below:

Fundraising challenges prompt greater diversification

Historically, many US managers opted against marketing their products in Europe as they felt it was too complicated, excessively rules-based and highly fragmented – a problem compounded by Brexit.

However, this long-held indifference towards Europe is now a thing of the past for a lot of US managers, especially as fundraising has become increasingly challenging.

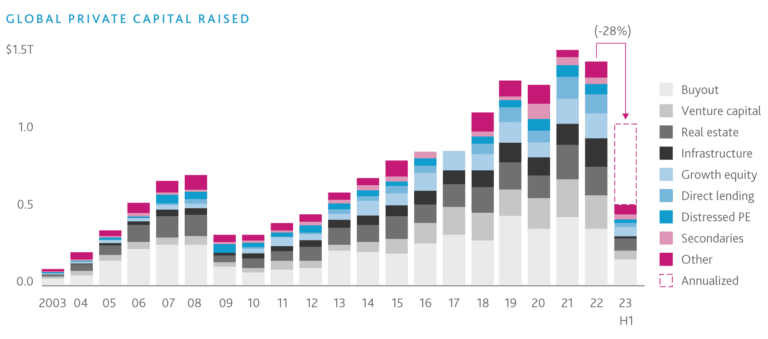

Sparked by the difficult market conditions, such as geopolitical tensions, equity market volatility, high inflation and rising interest rates, the $11.7 trillion1 private capital industry is finding it harder to compete for and attract new investors. Bain & Co’s Private Equity Mid-Year Report 2023 also showed the fundraising challenge, as highlighted in the table below.

Source: Bain & Co Stuck in place: Private Equity mid-year report 2023

This fundraising slowdown is having a disproportionate impact on US firms who make up the bulk of the private capital industry’s total assets under management (AuM). In response, we are now seeing more US managers start to diversify their client base by targeting European institutional investors.

Why Europe?

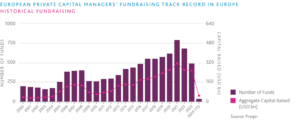

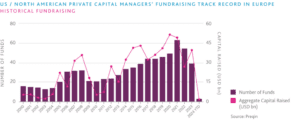

For many US managers, Europe’s investor market is an untapped commercial opportunity. Whereas Europe-based private capital managers accumulated an aggregate $252.8 billion in 2023 from European investors, US managers only captured $39.2 billion2.

Source: Preqin

The historical inclination towards European managers has not impeded US managers in seeking out Europe as a viable source of fresh capital for multiple reasons.

Firstly, there is an abundance of wealth in the region, which is heavily populated by institutional investors, such as sovereign wealth funds, pension funds and insurance companies, many of whom have seen their cash reserves increase substantially. Germany’s institutional investor market, for instance, has grown by 8.4% annually since 2013, and now sits on an asset pile totalling €3.4 trillion3.

Notwithstanding the recent downturn in private markets, European institutions are still showing confidence in the private capital industry, mainly because they crave portfolio diversification and alpha, following disappointing performance at many of their traditional money managers.

Targeting by region

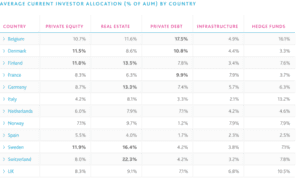

On a market-by-market basis, there is a clear partiality towards certain private capital strategies over others, as the table from Preqin below indicates4. This analysis can be a good tool for managers when deciding where their fundraising efforts should be targeted.

In terms of investor asset allocations, real estate appears to be one of the more popular private capital strategies, with institutions in Switzerland allocating on average nearly a quarter (22.3%) of their AuM to the asset class, followed by Sweden (16.4%), Finland (13.5%) and Germany (13.3%).

Private equity is also increasingly sought after, especially by institutions in the Scandinavian markets. The Preqin data shows that investors in Sweden on average allocated 11.9% of their AuM to private equity, followed by Finland (11.8%) and Denmark (11.5%).

Private debt is a rapidly expanding asset class, although investor allocations in Europe remain on the low side. Despite this, Belgium-based institutions invested nearly 17.5% of their overall AuM to private debt, followed by Denmark (10.8%), and France (9.9%).

According to a Coalition Greenwich study, 30% of European institutions plan to increase their exposures to private capital funds, led by private equity, infrastructure and private debt, over the next three years5.

Tapping into non-institutional capital

Outside of institutions, Europe’s high net worth investor (HNWI) market is fairly sizeable, and it is a demographic which private capital firms desperately want to tap into. The region’s HNWIs are also quite open to private capital investing, and are projected to increase their allocations over the next 12 to 24 months, as indicated by the chart below6.

It is therefore not surprising that US managers are increasingly targeting this region. However, to attract European investors, managers need more than just a compelling track record.

Identifying the right marketing strategy

Firstly, managers need to think carefully about their marketing strategy.

US private capital managers can access EU investors through one or more of the following channels:

- National Private Placement Regimes (NPPRs)

- By establishing an AIFM (Alternative Investment Fund Manager) themselves or using a third-party AIFM

- Reverse solicitation

Under the Alternative Investment Fund Managers Directive (AIFMD), US private capital managers can leverage the NPPR, which lets them register their fund(s) in a specific EU member state(s) for marketing purposes. Although NPPR is restricted in certain EU countries (e.g. France), this approach is a sensible one for managers to take, providing they are only targeting investors located in a handful of member states.

Alternatively, some managers may choose to either launch an AIFM or use a third-party AIFM ManCo, both of which enable managers to distribute their products on a pan-EU basis. Setting up an AIFM can be a costly process for managers, which is why so many choose to use third-party ManCos. A ManCo lets managers market their funds cross-border into the European member states without having to invest in the physical infrastructure that comes with running an AIFM. It also gives fund managers access to high-quality resources — people with hands-on portfolio management experience, risk management professionals and governance professionals. Alongside the requirement for an AIFM, each AIF will also need to appoint an independent depositary to safekeep the fund’s assets, perform oversight duties and monitor the fund’s cash flow.

For asset managers not yet established in Europe, pre-marketing has also become a popular solution for those wishing to perform cross-border marketing and are contemplating launching a European investment fund, as it gives the opportunity to test investors’ appetite for their strategies at a limited cost, provided that they are facilitated by an AIFM.

The final option is to rely on reverse solicitation.

This is loosely defined as when an investor directly and independently reaches out to a fund promoter seeking information about a fund. Despite its cost benefits – reverse solicitation has the potential to cause compliance issues, and only tends to benefit larger managers who have pre-existing relationships with European investors. However, even for larger managers ESMA has reminded the industry that solely depending on reverse solicitation is not a feasible marketing strategy7.

Consequences of relying solely on reverse solicitation could potentially include regulatory sanctions, loss of investor trust, reputational damage, and potential legal actions.

Choosing your structure

If a manager chooses the AIFM route, they have the freedom to domicile their fund in any EU jurisdiction. However, most non-EU managers targeting EU investors will usually domicile their funds onshore in one of either Ireland or Luxembourg, both of which offer suitable and tested fund structures and have a local services industry with extensive experience in fund structuring and fund servicing. It is important, nevertheless, to understand the preferences of the underlying investor base before settling on a jurisdiction and structure for a fund.

Ireland

Ireland is now the third largest investment fund centre in the world, and the second largest in Europe (behind Luxembourg). The major benefit of Ireland as a fund domicile of choice is the full funds product coverage across UCITS, AIFs, ETFs and private equity. It also offers full access and passporting capabilities to the EU, which is essential for fund distribution. In addition, there is a good network of double taxation treaties, including with the US.

One of the more popular models for private equity fund managers is the Irish Limited Partnership (ILP). ILPs, which can be established as Qualifying Investor AIFs, are easy to set up, tax transparent and regulated by the Central Bank of Ireland (CBI), enabling managers to market their products seamlessly across EU member states.

Luxembourg

Meanwhile, Luxembourg remains the second largest funds destination in the world behind the United States due to its stability, adaptability, investor friendly eco system and choice of fund structures. The most popular vehicle when establishing a private equity fund in Luxembourg is the Reserved Alternative Investment Fund (RAIF). One of the features of this structure that has led to the rise in popularity is it does not require managers to obtain approval from the local regulator, the Commission de Surveillance du Secteur Financier (CSSF) (meaning it can be set up within a few weeks), nor is it subject to ongoing CSSF supervision. There are also a large range of corporate structures available, including the FSP, SICAV, and SCS and SCSp. They can also make use of umbrella structures, enabling them to launch ring-fenced sub-funds which correspond to distinct assets and liabilities.

ELTIFs

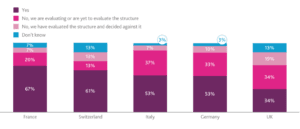

More recently, private capital managers have been exploring the merits of whether to launch a European Long Term Investment Fund (ELTIF). Typically domiciled in Ireland or Luxembourg, ELTIFs provide the ability to market to both retail and professional investors, a significant advantage over other AIFs which can only be marketed to professional investors. This is especially important given recent fundraising challenges.

Owing to its semi-liquid nature and following recent improvements by EU regulators to the ELTIF framework under ELTIF 2.0, including the easing of restrictions on investing into non-EU assets and removing unnecessary barriers for entry, ELTIFs seem to be generating renewed interest.

Source: Cerulli Associates8.

Private banks and wealth managers: Views on investing in or offering ELTIFs, 2023. Analyst note: Respondents were asked if their firms invest in or plan to offer ELTIFs to their clients.

The Channel Islands are also an equally attractive fund domicile. Both Jersey and Guernsey adopt a regulatory framework, which is proportionate and flexible. In addition to letting private capital firms market into the EU via NPPR, managers domiciled in the Channel Islands can also reach out to investors outside of the EU, including in the UK.

Choosing the right fund structure and domicile will be absolutely critical for US managers raising capital in Europe.

The next frontier for US managers

European investors are chasing new sources of returns, and many are now leaning towards private capital strategies. At the same time, a number of US private capital managers – following a marginal decline in fundraising – want to broaden their distribution footprints in Europe, having previously eschewed the region.

Competition for assets is high in today’s market and many investors are looking at more than just performance from their managers. A well-planned fund structure and an intelligent distribution model will be essential if US private capital managers are to attract and win mandates in Europe.

If you would like to discuss this article in detail or find out more about JTC’s services please contact Wouter, Dewi or Stephanie directly.

1McKinsey. Published March 21, 2023. McKinsey Global Private Markets Review: Private markets turn down the volume.

2Preqin data.

3Universal Investment. Published December 13, 2023. What is the scale and opportunity of the German market?

4Preqin data.

5Bloomberg. Published December 13, 2023. European institutions plan more investments in private markets.

6EFAMA. Published December, 2023. An overview of the asset management industry.

7https://www.esma.europa.eu/press-news/esma-news/esma-reminds-firms-mifid-ii-rules-reverse-solicitation

8Private banks and wealth managers: Views on investing in or offering ELTIFs, 2023. Analyst note: Respondents were asked if their firms invest in or plan to offer ELTIFs to their clients.

Key contact

Stay Connected

Stay up to date with expert insights, latest updates and exclusive content.

Discover more

Stay informed with JTC’s latest news, reports, thought leadership, and industry insights.

Let’s Bring Your Vision to Life

From 2,500 employee owners to 14,000+ clients, our journey is marked by stability and success.